CLL1M Index

CLL1M Index Dashboard, CLL1M Dashboard

Index Dashboard

- CLL1M

Cboe S&P 500 Risk Managed Income Index

- Overview

- Performance

The Cboe S&P 500 Risk Managed Income Index is a passive strategy which consists of(a) holding the S&P 500 portfolio and collecting dividends,(b) buying 5% out-of-the-money SPX puts that expire on the monthly cycle, and(c) selling at-the-money SPX calls that expire on the monthly cycle.The options are “rolled” at SPX expirations, usually on the third Friday of the month.

Resources

- Cboe Collar Indices Methodology

- Click here to see the complete roll data.

Cboe CLL1M Index Roll Information - March 21, 2025

| Index | Name | Reference Price | New Put Strike Price | New Call Strike Price | New Put VWAP Price | New Call VWAP Price | Underlying Index VWAP |

|---|---|---|---|---|---|---|---|

| CLL1M | Cboe S&P 500 Risk Managed Income Index | 5637.51 | 5360 | 5640 | 31.39367088607595 | 115.69495586380833 | 5637.542966582598 |

Cboe CLL1M Index Roll Information - February 21, 2025

| Index | Name | Reference Price | New Put Strike Price | New Call Strike Price | New Put VWAP Price | New Call VWAP Price | Underlying Index VWAP |

|---|---|---|---|---|---|---|---|

| CLL1M | Cboe S&P 500 Risk Managed Income Index | 6081.8 | 5780 | 6085 | 21.481333333333332 | 82.93226005238022 | 6066.516646125404 |

Cboe CLL1M Index Roll Information - January 17, 2025

| Index | Name | Reference Price | New Put Strike Price | New Call Strike Price | New Put VWAP Price | New Call VWAP Price | Underlying Index VWAP |

|---|---|---|---|---|---|---|---|

| CLL1M | Cboe S&P 500 Risk Managed Income Index | 6002.99 | 5705 | 6005 | 21.69722222222222 | 104.63460095497953 | 6009.089554911324 |

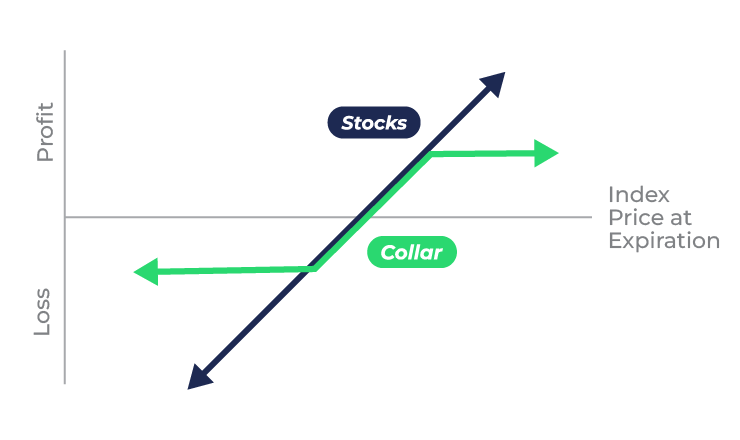

Collar Strategy

Goals

The goal of the index options collar strategy is to provide a floor for the downside risk for a portfolio of stocks, and reduce net out-of-pocket hedging costs, in exchange for an upside cap.

Strategy

To implement an index collar strategy: (1) buy or hold a portfolio of stocks, (2) buy out-of-the-money index protective put options to hedge the portfolio, and (3) sell out-of-the-money index covered calls with the same expiration as the index puts.

Comments

The premium income received from the sale of the calls can help offset the cost of the index puts. The long index puts establish a downside floor, the short index calls establish an upside ceiling or cap, and the position is collared between the floor and the ceiling.